Last month's introduction of the AI Incident Reporting Act didn't make many headlines, but it should. The proposed law would require AI developers to report serious incidents to the Department of Commerce within seven days—48-hour notices for anything posing imminent risk.

Your agency is probably already running AI tools for underwriting, claims triage, or customer service. Maybe it's a chatbot handling certificate requests, an underwriting platform flagging high-risk commercial accounts, or that claims routing system you stood up last quarter.

Each one becomes a potential compliance problem.

The vendor problem nobody's talking about

What makes this genuinely complicated for insurance agencies is that you don't control the AI systems you depend on.

When Applied Epic rolls out an AI feature update, you take it. When your claims platform adds machine learning to speed up triage, you adapt. When that insurtech startup you partnered with tweaks their algorithm, you trust it works.

Under the proposed AI incident reporting compliance framework, those vendors would be responsible for tracking and reporting incidents that affect your operations. But their definition of "incident" might not line up with what actually matters to your agency. A vendor might consider a 2% accuracy drop acceptable while you're dealing with commercial clients whose claims got misrouted.

This exact scenario played out at a mid-sized agency in Phoenix recently. Their AI-powered claims platform pushed a "minor update" that started routing workers' comp claims to the wrong adjusters. The vendor didn't classify it as reportable because the system was technically still running. The agency, meanwhile, had seventeen commercial accounts threatening to walk because claims that should've resolved in 48 hours were sitting untouched for a week.

The vendor's incident log showed nothing. The agency's E&O exposure was significant.

Mapping your actual AI dependencies

Most agencies undercount their AI touchpoints by a wide margin.

Eliminate paperwork bottlenecks and missed deadlines.

Covixly helps you track, manage, and close every policy and claim with confidence and speed.

- Unified policy & claims management

- Automated client notifications

- Agent task coordination

No credit card required

You think you have three or four AI tools. Run a proper inventory and you'll typically find closer to twelve or fifteen. That quote comparison tool uses AI. Your email system has AI filtering. Document extraction for certificates runs on machine learning. Even your phone system probably routes calls using some form of AI now.

Start with this breakdown:

Direct AI Systems

-

Underwriting platforms with risk scoring

-

Claims triage and routing systems

-

Customer service chatbots

-

Document processing tools

-

Quote generation platforms

Hidden AI Components

-

CRM predictive features

-

Email priority filtering

-

Call routing algorithms

-

Fraud detection modules

-

Renewal prediction models

Third-party AI Services

-

Carrier platforms you access

-

MGA tools and portals

-

Vendor management systems

-

Marketing automation

-

Data enrichment services

One agency discovered their "simple" certificate generation tool actually pulled from four different AI services: document extraction, data validation, template matching, and quality checking—each from a different vendor. Under the proposed reporting rules, that's four potential failure points with different incident thresholds and reporting timelines.

Building your incident response framework

The agencies that get through AI incident reporting compliance won't be the ones with perfect systems. They'll be the ones with clear escalation paths when things break.

Right now, your incident response probably looks like this: system goes down, everyone panics, IT scrambles, someone eventually emails clients about "technical difficulties." That approach won't hold up when AI incidents trigger federal reporting requirements and potential liability claims.

A functional framework needs three layers:

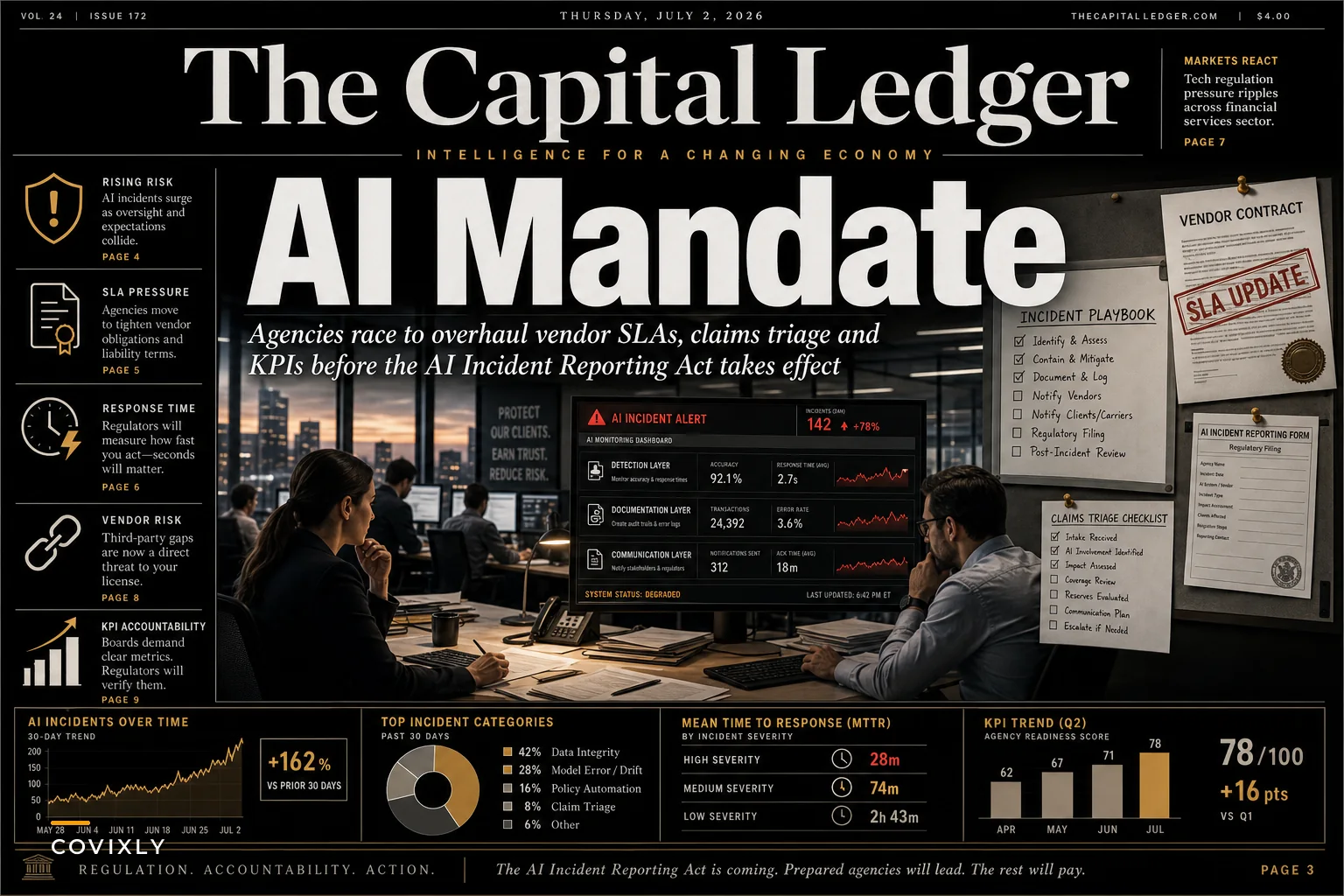

Detection Layer You need to catch AI system failures before clients do. Monitor accuracy rates, response times, and output patterns. Set thresholds that reflect your agency's risk tolerance, not vendor defaults.

Documentation Layer Every AI-related issue needs a paper trail. Not "system was slow Tuesday morning" but specific details: which processes failed, how many transactions were affected, what errors appeared, which clients were impacted.

| Layer | Details |

|---|---|

| Detection Layer | You need to catch AI system failures before clients do. Monitor accuracy rates, response times, and output patterns. Set thresholds that reflect your agency's risk tolerance, not vendor defaults. |

| Documentation Layer | Every AI-related issue needs a paper trail. Not "system was slow Tuesday morning" but specific details: which processes failed, how many transactions were affected, what errors appeared, which clients were impacted. |

| Communication Layer | Different incidents require different responses. A chatbot giving wrong business hours needs a quick client notice. An underwriting AI missing exclusions might trigger E&O protocols. Claims routing failures could require carrier notifications. |

Here's a simple workflow to visualize escalation paths.

Set thresholds that reflect your agency's real risk tolerance, not vendor defaults.

Communication Layer Different incidents require different responses. A chatbot giving wrong business hours needs a quick client notice. An underwriting AI missing exclusions might trigger E&O protocols. Claims routing failures could require carrier notifications.

The claims triage nightmare scenario

Claims processing concentrates every AI incident reporting risk in one workflow.

Your triage system pulls data from multiple sources, makes routing decisions based on learned patterns, and directly affects client outcomes. When it fails—and it will—you're dealing with operational, compliance, and liability issues at the same time.

Picture this chain of events:

-

AI misclassifies a commercial property claim as personal lines

-

Claim routes to the wrong adjuster queue

-

Commercial client's contractor can't start repairs

-

Business interruption coverage questions surface

-

Client files a complaint with the state insurance department

-

Your E&O carrier wants documentation you don't have

Under the proposed reporting requirements, that same incident might trigger vendor obligations to report the AI failure to federal authorities. You won't know if they reported it, what they said, or how it affects your agency's liability position.

Vendor contracts need immediate attention

Pull any SaaS contract from 2022 or earlier and search for "artificial intelligence," "machine learning," or "algorithm." You'll find almost nothing—maybe a vague mention of "technology" or "systems," but nothing about incident reporting, federal compliance, or liability allocation when AI fails.

Analysis from CSO Online notes the proposed law creates specific timelines and thresholds vendors must follow. Your contracts need to spell out:

-

Who determines if an incident is reportable

-

How vendors notify you of reported incidents

-

What documentation you receive

-

How liability splits between parties

-

Who handles client communications

-

What happens to your data during investigations

Start with your highest-risk vendors—anyone touching claims, underwriting, or compliance. Add specific AI incident language to renewals. Don't hold out for perfect templates. Get something on paper now.

Practical compliance steps without the panic

The agencies handling this best aren't standing up massive compliance departments. They're making targeted adjustments to existing processes.

Week 1–2: Inventory and Classify List every system with AI components. Note which ones affect regulated activities like underwriting and claims. Flag anything that handles sensitive data or makes autonomous decisions. This becomes your risk priority list.

Week 3–4: Update Documentation Modify your existing incident logs to capture AI-specific details. Add fields for algorithm versions, training data dates, accuracy metrics, and decision explanations. Your CSRs need a simple way to flag "AI weirdness" without needing to understand the technical side.

Month 2: Vendor Conversations Schedule calls with your top five AI vendors. Ask direct questions about their incident reporting plans. Get written responses about how they're interpreting compliance obligations. Many vendors haven't thought this through yet—your questions might push them to start.

Month 3: Process Updates Fold AI monitoring into existing workflows. Claims managers already track processing times—add AI accuracy checks. Underwriters already review declined applications—add AI decision audits. Compliance officers already handle state reporting—add AI incident tracking.

The operational overhaul nobody wants to discuss

Beyond compliance, this changes how you evaluate and implement AI tools going forward.

That platform promising 50% faster claims processing? Now you need to assess their incident reporting infrastructure. The startup offering underwriting assistance? Better check their federal compliance readiness.

This effectively ends the "move fast and break things" approach to AI adoption in insurance. Agencies will need staged rollouts, parallel processing periods, and fallback procedures for every AI-enhanced workflow.

Some agencies will use this as a reason to avoid AI entirely. That's the wrong call. The efficiency gains are real and significant—agencies still running fully manual processes are going to get outpaced. The answer isn't avoiding AI; it's building operational frameworks that treat AI failures as routine events rather than emergencies.

Creating your AI incident playbook

A working playbook beats a perfect policy document every time.

Start with scenarios your agency faces regularly, then map the AI failure modes:

Scenario: Auto claim filed Sunday night

-

Normal flow

AI triages to appropriate adjuster Monday morning

-

Failure mode

AI misreads damage description, routes to wrong department

-

Detection

Adjuster flags incorrect routing Monday afternoon

-

Response

Immediate reroute, client notification of delay, log AI error

-

Follow-up

Vendor notification, accuracy audit, process adjustment

Scenario: Commercial renewal quote request

-

Normal flow

AI pulls policy history, generates renewal options

-

Failure mode

AI misses recent claims, quotes incorrect premium

-

Detection

Underwriter catches error during review

-

Response

Manual requote, client explanation, document AI failure

-

Follow-up

Vendor escalation, E&O review, training data flag

Build five to seven scenarios that match your agency's actual volume patterns. Run tabletop exercises regularly. Get your team comfortable with the phrase "AI incident" before it becomes a federal reporting trigger.

The connection to existing compliance challenges

Agencies already navigating compliance automation for high-risk commercial policies are dealing with compounded pressure. The same complex commercial accounts that break rule-based systems will generate the most AI incidents.

Your AI struggles most with unusual risks, extensive schedules, and non-standard coverage—exactly the policies that already require manual intervention. Adding federal reporting requirements when AI fails to handle these accounts creates layered complexity for agencies that haven't built exception-handling processes yet.

Agencies that already track when automation breaks down, have escalation procedures, and document edge cases are better positioned. Extending those frameworks to cover AI incident reporting is an update, not a rebuild.

Preparing without overreacting

The AI Incident Reporting Act might pass as written, get heavily amended, or stall entirely. As Reuters reported, the legislative path remains unclear. But the direction isn't ambiguous: AI systems will face increasing scrutiny and reporting requirements regardless of what this specific bill does.

Build flexibility into your AI governance rather than optimizing for one regulatory outcome. Create monitoring systems adaptable to different reporting thresholds. Develop vendor relationships that can survive regulatory changes.

Agencies that waited for final data breach notification rules before building incident response capabilities got caught scrambling. The ones that built those capabilities early barely noticed when the rules went live.

Your operational software should make this easier. Modern platforms built for insurance workflows can track AI decision points, flag anomalies, and maintain audit trails without constant manual input. The difference is whether compliance monitoring was designed in from the start or patched on after something went wrong.

What happens next

Over the next several months, watch for three things:

Established insurtech vendors will start announcing their AI incident reporting positions. The bigger players will move first, probably overbuilding their responses. Smaller vendors will scramble.

State insurance departments will issue guidance on AI in regulated activities before federal legislation lands. California, New York, and Illinois are likely to move first with "recommendations" that carry the practical weight of requirements.

E&O carriers will update policy language around AI-related incidents. Some will exclude AI failures outright. Others will require specific AI governance documentation. Expect AI risk assessments to become part of renewal conversations.

Agencies getting ahead of this now—updating contracts, building monitoring processes, training staff—will handle these changes without much disruption. The ones hoping it goes away will face compressed timelines and compliance scrambles.

Start with the basics: know what AI you use, document when it fails, and maintain clear vendor accountability. Everything else builds from that foundation.

Ready to transform your insurance agency operations?

Join 500+ agencies using Covixly to reduce manual work, improve client service, and grow their book of business.