You know that feeling when a new commercial account with 47 vehicles and three locations lands on your desk at 4pm on Thursday? Or when personal lines is drowning in quote requests while your senior CSR is out sick?

Most agencies handle onboarding like they're defusing a bomb – carefully, slowly, and praying nothing explodes. But the agencies who scale successfully treat onboarding like a production line, not an art project.

The difference between agencies stuck at $2M revenue and those breaking through to $5M+? They stopped treating every new client like a unique snowflake and built repeatable systems that work under pressure.

Why personal and commercial lines need completely different playbooks

Trying to force commercial accounts through the same process as someone buying auto insurance is like using a sedan to haul construction equipment – technically possible, but painful for everyone involved.

Personal lines onboarding is about speed and volume. You're processing 15-20 new households per week, each needing maybe 2-3 policies. The whole thing should take 24-48 hours from first contact to bound coverage. Most of the work is data entry, quote comparison, and basic coverage education.

Commercial lines? That's a different animal. You might onboard 2-3 new commercial accounts per month, but each one involves multiple stakeholders, complex coverage analysis, often 5-10 different policies, and weeks of back-and-forth. Miss a certificate holder on a contractor's GL policy and you'll hear about it when they can't start that job next Monday.

Personal lines needs automation and templates. Commercial lines needs checkpoints and human judgment. Mix them up and you get personal lines clients waiting three weeks for auto quotes, or commercial accounts with coverage gaps because someone rushed through the process.

Personal lines onboarding: the 48-hour sprint

Day 1 checklist (0-24 hours from initial contact)

Eliminate paperwork bottlenecks and missed deadlines.

Covixly helps you track, manage, and close every policy and claim with confidence and speed.

- Unified policy & claims management

- Automated client notifications

- Agent task coordination

No credit card required

Initial contact processing (2-4 hours)

-

Capture basic info through your intake form

-

Run MVR and CLUE reports

-

Quote with at least 3 carriers

-

Schedule follow-up within 24 hours

-

Send automated welcome email with next steps

Document collection (parallel process)

-

Current dec pages (if switching carriers)

-

Driver's licenses for all household members

-

Vehicle registrations

-

Mortgage info for homeowners

-

Prior insurance proof (for continuous coverage discount)

The trick is parallel processing. While your CSR runs reports, your automation should collect documents through a portal. No back-and-forth emails, no "can you send that again" – just a simple upload link that tracks what's missing.

Day 2 execution (24-48 hours)

Coverage review and binding

-

Present quote comparison (15-minute call)

-

Explain coverage differences

-

Get payment method

-

Bind coverage

-

Send all policy documents

-

Set up automatic payments

-

Schedule 6-month review

Post-binding tasks

-

Cancel prior policies (with overlap date confirmed)

-

Update mortgagee if applicable

-

Send ID cards

-

Add to renewal tracking

-

Trigger welcome sequence

What kills efficiency is the coverage review call. Keep it to 15 minutes. Use a standard comparison sheet that highlights the three things that actually matter: price, deductibles, and liability limits. Everything else can be handled in the welcome materials.

Keep it to 15 minutes. Use a standard comparison sheet that highlights the three things that actually matter: price, deductibles, and liability limits.

Decision rules for personal lines automation

Not every personal lines client needs the full touch treatment. Here's when to automate vs when to escalate:

Fully automate when:

-

Standard auto/home bundle

-

Clean driving records (no violations in 3 years)

-

Continuous coverage

-

Credit score above 650

-

No claims in past 5 years

-

Property built after 1980

Require human review when:

-

Multiple violations or claims

-

Coverage gaps

-

Non-standard risks (trampolines, certain dog breeds)

-

High-value homes (over $750k)

-

Multiple locations or vehicles (5+)

-

Business use vehicles

Immediate escalation triggers:

-

Prior carrier non-renewal

-

SR-22 requirement

-

Vacant property

-

Short-term rental use

-

Home-based business with liability exposure

The point isn't to automate everything – it's to automate what's predictable so your team can focus on the exceptions that actually need expertise.

Commercial lines onboarding: the strategic operation

Week 1: discovery and data gathering

Initial commercial assessment (Day 1-2)

-

Business structure and ownership

-

Revenue and payroll by class code

-

Location details and square footage

-

Vehicle schedule with usage

-

Contractual requirements

-

Current coverage and premiums

-

Loss history (5 years)

Exposure identification checklist

-

General liability limits and additional insureds

-

Property values and business personal property

-

Auto fleet and hired/non-owned exposure

-

Workers comp class codes and experience mod

-

Professional liability needs

-

Cyber liability assessment

-

Umbrella limits evaluation

The biggest mistake agencies make is rushing through exposure identification. That landscaping company might also plow snow in winter (completely different GL class). That restaurant might cater off-premise events (liquor liability nightmare). That contractor might do residential work (needs different coverage than commercial-only).

Week 2: market approach and negotiation

Carrier submission package

-

Completed ACORD applications

-

Supplemental applications by line

-

Loss runs (valued and typed)

-

Financial statements (if over $5M revenue)

-

Safety programs and procedures

-

Photos of property and operations

Market management rules

-

Submit to no more than 5 carriers initially

-

Block markets strategically

-

Get quotes back within 5 business days

-

Follow up daily after day 3

-

Have backup markets identified

What separates good commercial producers from great ones? They manage markets like a chess game. Submit to too many carriers and you'll burn markets. Too few and you won't get competitive pricing. The sweet spot is usually 3-4 primary markets plus 1-2 specialty carriers for unique exposures.

Week 3-4: presentation and binding

Proposal preparation standards

-

Side-by-side coverage comparison

-

Premium breakdown by line

-

Payment options and fees

-

Coverage gap analysis

-

Recommended enhancements

-

Implementation timeline

Binding checklist

-

Signed applications (all lines)

-

Down payment collected

-

Additional insured endorsements ordered

-

Certificate holders documented

-

Waiver of subrogation noted

-

Loss payees added

-

Audit contact designated

Most agencies lose commercial accounts before they even start: the handoff from sales to service. The producer closes the deal, throws it over the wall to service, and suddenly the client is calling asking why their certificate isn't right. Build in a formal handoff meeting – 30 minutes that saves hours of scrambling later.

SLA targets that actually improve operations

Realistic SLA targets by task

Personal lines response times

-

New quote request

4 business hours

-

Policy change

Same business day

-

Claims reporting

Within 1 hour

-

Payment question

Same business day

-

Renewal review

30 days before expiration

-

Cancellation processing

Within 24 hours

Commercial lines response times

-

New submission

24-hour acknowledgment

-

Full quote

5-7 business days

-

Certificate request

4 business hours

-

Policy change

24-48 hours

-

Audit assistance

48 hours

-

Renewal proposal

60 days before expiration

| Task | Target |

|---|---|

| New quote request | 4 business hours |

| Policy change (personal) | Same business day |

| Claims reporting | Within 1 hour |

| Full quote (commercial) | 5-7 business days |

| Certificate request | 4 business hours |

| Renewal proposal (commercial) | 60 days before expiration |

Measuring what matters

Personal lines KPIs

-

Time to quote

Target under 4 hours

-

Quote to bind ratio

Target 25-35%

-

Onboarding completion

Target 48 hours

-

First-call resolution

Target 80%

Commercial lines KPIs

-

Submission to quote

Target 5 days

-

Quote to bind ratio

Target 40-50%

-

Renewal retention

Target 90%+

-

Certificate accuracy

Target 95% first-time-right

The numbers tell you where your process breaks. If quotes take 3 days instead of 4 hours, you're losing personal lines to online carriers. If commercial certificates need constant corrections, you're burning service hours on preventable rework.

Building escalation paths that prevent disasters

Personal lines escalation triggers

Level 1 (CSR handles)

-

Standard coverage questions

-

Payment plan options

-

Basic underwriting clarifications

-

Document collection follow-ups

Level 2 (Senior CSR/Account Manager)

-

Coverage gaps or exclusions

-

Price objections over 20%

-

Non-standard risks

-

Underwriting exceptions needed

Level 3 (Producer/Principal)

-

Declined by multiple carriers

-

High-value account (over $5k premium)

-

Service complaints

-

Legal or regulatory issues

Commercial lines escalation framework

Risk-based escalation

-

Under $10k premium

Account manager handles fully

-

$10k-50k premium

Producer reviews before binding

-

Over $50k premium

Principal involvement required

-

New industry/class

Team discussion before quoting

Issue-based escalation

-

Coverage disputes

Producer within 2 hours

-

Audit problems

CFO or operations manager

-

Claims issues

Producer and principal

-

Non-renewal threats

Principal immediately

Escalation isn't about punting problems upward – it's about getting the right expertise involved before small issues become account-threatening problems.

Quality control checkpoints that save accounts

Most agencies discover problems when the client calls angry. Build checkpoints that catch issues before they matter.

Personal lines quality checks

Pre-bind verification

-

Coverage matches quoted limits

-

All drivers listed

-

All vehicles included

-

Discounts applied correctly

-

Payment plan confirmed

24-hour post-bind

-

Documents sent successfully

-

Prior carrier cancellation scheduled

-

Mortgagee updated

-

Client portal access working

30-day follow-up

-

First payment processed

-

ID cards received

-

Questions from documents

-

Additional coverage needs

Commercial lines verification points

Before sending quotes

-

All exposures identified

-

Class codes correct

-

Territory ratings accurate

-

Experience mods applied

-

Minimum premiums understood

Before binding

-

Additional insureds listed

-

Certificate requirements confirmed

-

Endorsements documented

-

Audit contacts designated

-

Payment terms agreed

Week 1 after binding

-

Certificates issued correctly

-

Policies received and reviewed

-

Invoicing set up properly

-

Service team fully briefed

Most agencies discover problems when the client calls angry. Build checkpoints that catch issues before they matter.

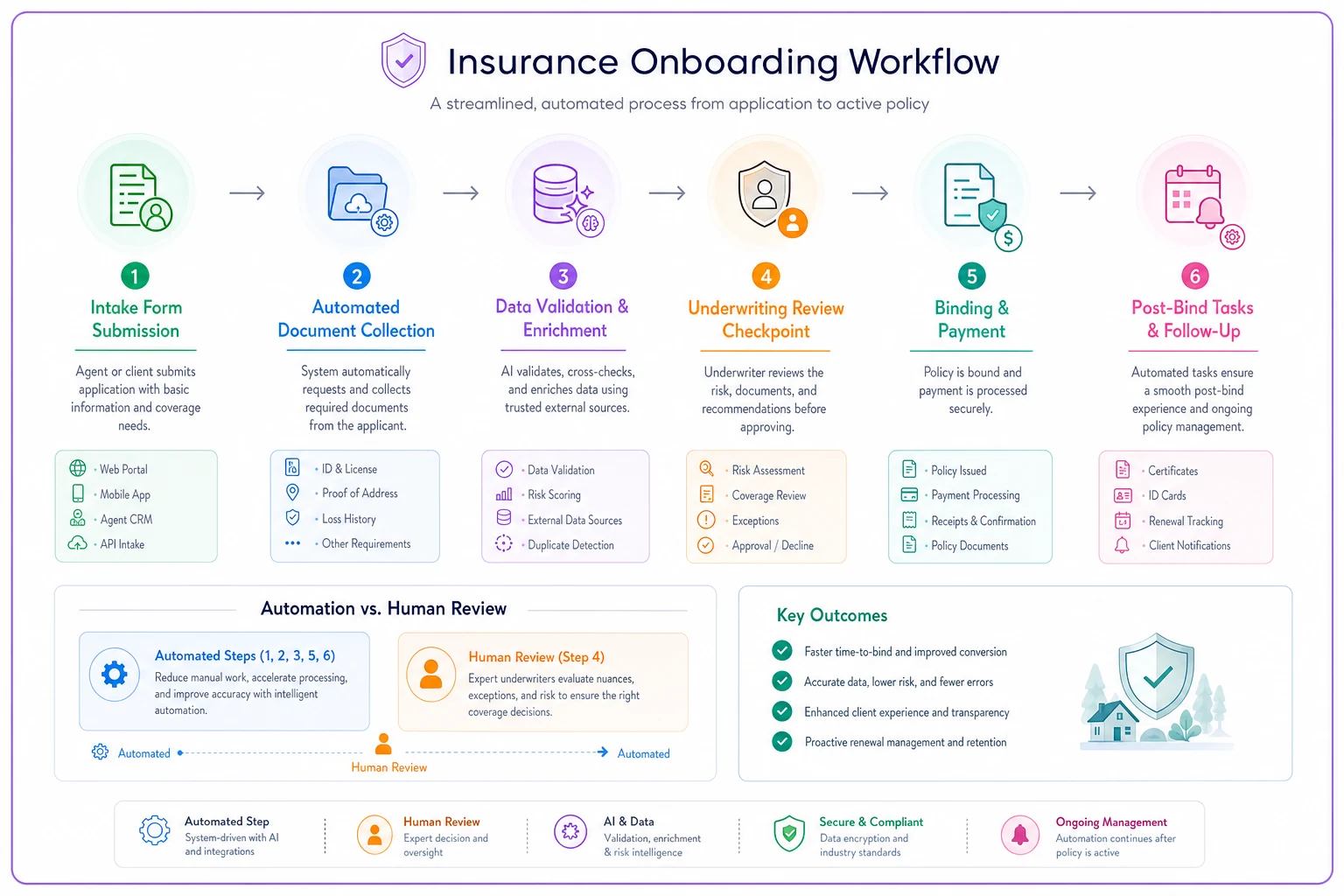

Technology integration that actually helps

AI-powered operational software becomes genuinely useful here – not as magic, but as infrastructure that handles the predictable stuff so humans can focus on what matters.

Good onboarding software should do three things:

First, it captures information once and populates it everywhere. No retyping the same business name seventeen times across different applications. The AI handles the data flow while your team handles the decisions.

Second, it tracks where everything stands without constant status meetings. You can see instantly which accounts are waiting on documents, which need underwriting approval, which are ready to bind. The operational transparency alone saves hours of internal communication.

Third, it enforces your process without being rigid. The system guides new staff through the right steps while letting experienced people skip what they don't need. Think guardrails, not handcuffs.

The agencies that scale successfully use automation to handle data movement and process enforcement, freeing their people to handle relationship building and complex problem-solving. It's not about replacing humans – it's about not wasting human talent on robotic tasks.

A visual workflow helps align the team on where automation should act and where human judgment is required.

This illustrates how automation handles routine tasks and when humans should intervene.

Common failure points and prevention

The patterns become obvious after watching hundreds of onboarding processes fail.

The documentation black hole: Documents get requested, clients send them to personal emails, things get lost, nobody knows what's missing. Solution: One portal, automatic tracking, clear status for everyone.

The handoff fumble: Sales sells something, service delivers something different, client gets confused and angry. Solution: Documented handoff meeting with checklist, not casual conversation.

The coverage assumption: Someone assumes the client wants the same coverage as before, skips the conversation, misses that they just bought a boat. Solution: Mandatory coverage review questions, even for renewals.

The timeline creep: Commercial account needs binding by Friday for a Monday job start, but nobody communicated urgency. Solution: Capture deadlines upfront, build the timeline backward.

The payment surprise: Client thinks they're paying monthly, gets hit with a huge down payment, deals falls apart. Solution: Payment discussion before running quotes, not after.

These aren't complicated problems. They're coordination and communication failures that happen when you don't have clear processes. Fix the process, fix the problem.

Measuring success and continuous improvement

Your onboarding process is either getting better or getting worse – it never stays the same.

Track time-to-completion by line of business. Personal lines should trend toward 24 hours. Commercial lines should stabilize around 10-15 business days. If times are increasing, you've got a bottleneck to find.

Monitor abandonment rates. Where do prospects fall out of your process? If 30% never provide documents after the quote, your document request process needs work. If 40% ghost after the coverage review call, you're probably overwhelming them with options.

Check accuracy rates. How often do you need to fix something after binding? Every correction is a sign that something in your process isn't clear enough.

Survey new clients at 30 days. Not a 47-question form – just three questions: How was the process? What was confusing? What would you change? The patterns in their answers will show you exactly where to improve.

Making this work in your agency

The playbook only works if your team actually uses it.

Start with one line of business. Get personal lines humming before tackling commercial, or vice versa. Trying to fix everything at once guarantees you'll fix nothing.

Document your current process first, however messy. You can't improve what you don't understand. Have your team walk through their actual steps, not what the manual says they should do.

Build your checklists together. The people doing the work know where it breaks. Let them help design the solution and they'll actually use it.

Test with new business only. Don't disrupt existing accounts while you're working out the kinks. Once the process is smooth, you can migrate existing clients during renewal.

Measure weekly, adjust monthly. Check your KPIs every week, but don't change the process constantly. Give changes time to work before tweaking again.

The agencies that win long-term aren't the ones with perfect processes – they're the ones that consistently improve their operations, month after month. This playbook gives you the framework. Your team's experience makes it work.

The difference between agencies that scale and agencies that struggle isn't talent or market opportunity. It's the boring stuff – the processes, the checklists, the systems that let talented people focus on what matters instead of reinventing the wheel every time a new client walks through the door.

Ready to transform your insurance agency operations?

Join 500+ agencies using Covixly to reduce manual work, improve client service, and grow their book of business.