Most insurance agencies think they have a policy lifecycle management problem when what they really have is a coordination nightmare spread across five different roles, three software systems, and about twelve Excel sheets that nobody trusts anymore.

The pattern becomes obvious after working with dozens of agencies. The ones that grow past 15 employees without constant fires aren't the ones with better agents or fancier CRMs. They're the ones who figured out that policy lifecycle management for insurance agencies isn't about managing policies—it's about managing the invisible handoffs between people who rarely talk to each other.

A commercial lines prospect gets quoted by your senior agent. The quote needs underwriter review, so it sits in someone's email for three days. The underwriter approves with conditions, but those conditions get buried in a reply-all chain. Your CSR processes the binding without seeing the conditions. Two months later, you're dealing with an E&O claim because nobody owned the handoff.

That scenario plays out in variations across every agency processing more than 200 policies monthly. The fix isn't more meetings or better communication. It's building an operational blueprint that makes responsibilities crystal clear and handoffs impossible to miss.

Why traditional policy management falls apart at scale

The standard agency playbook looks reasonable on paper. Agents sell, CSRs service, underwriters review complex risks, processors handle documentation, and account managers maintain relationships. Clean divisions, clear roles.

That's not how work actually flows through an agency.

A renewal comes in for a commercial property account. The account manager sees it needs remarketing because premiums jumped 30%. They hand it to an agent who's already working three other remarkets. The agent gets a better quote but needs underwriting approval for a coverage change. While waiting, the renewal date passes, the client calls angry, and suddenly everyone's in emergency mode trying to figure out who dropped what.

The fundamental problem is that policy lifecycle management treats each policy like it exists in isolation. But in reality, every policy touches multiple people at different stages, and those touchpoints multiply as you grow.

A 5-person agency can handle this through proximity and constant communication. Everyone knows what everyone else is working on. Once you hit 12-15 people, that informal coordination completely breaks down. You get duplicate work, missed handoffs, and nobody knowing who's supposed to do what.

The agencies that scale successfully don't do it by hiring better people or buying better software. They do it by acknowledging that policy lifecycle management is actually workflow orchestration across multiple roles, and they build their operations accordingly.

The five critical roles (and where their boundaries blur)

Role confusion kills more agency operations than any technology problem ever could.

Eliminate paperwork bottlenecks and missed deadlines.

Covixly helps you track, manage, and close every policy and claim with confidence and speed.

- Unified policy & claims management

- Automated client notifications

- Agent task coordination

No credit card required

Producers/Agents own new business and remarketing. Sounds simple until you realize they're also pulled into renewal negotiations, coverage disputes, and "quick questions" from long-time clients. Without clear boundaries, your highest-paid people spend half their time on $50/hour work.

Customer Service Representatives technically handle routine service requests. In practice, they become the catch-all for everything that doesn't fit elsewhere. Policy changes, billing questions, claim status updates, certificate requests—it all lands on their desk. The good CSRs learn to triage and route. The rest become bottlenecks.

Underwriting Assistants (in larger agencies) pre-screen submissions and handle routine endorsements. This role exists because someone finally realized that having $150k producers format ACORD applications is insane. But without clear escalation rules, they either bother underwriters constantly or make decisions beyond their authority.

Account Managers maintain relationships with larger accounts. They're supposed to be strategic, but they often get dragged into transactional work because clients call them directly. A good account manager on a 300-account book spends maybe 20% of their time on actual relationship building.

Processors/Policy Administrators ensure accuracy in policy issuance and documentation. They catch the errors everyone else makes. But they're usually the last to know about changes, working from outdated information while everyone wonders why policies take so long to issue.

The real problem isn't the roles themselves—it's the gaps between them. Every gap becomes a place where work disappears for days.

Building enforceable handoff rules that actually work

Handoff rules fail because agencies write them like suggestions instead of systems.

"Make sure to notify processing when binding" isn't a handoff rule. It's a hope. Real handoff rules have three components: a trigger, an action, and verification.

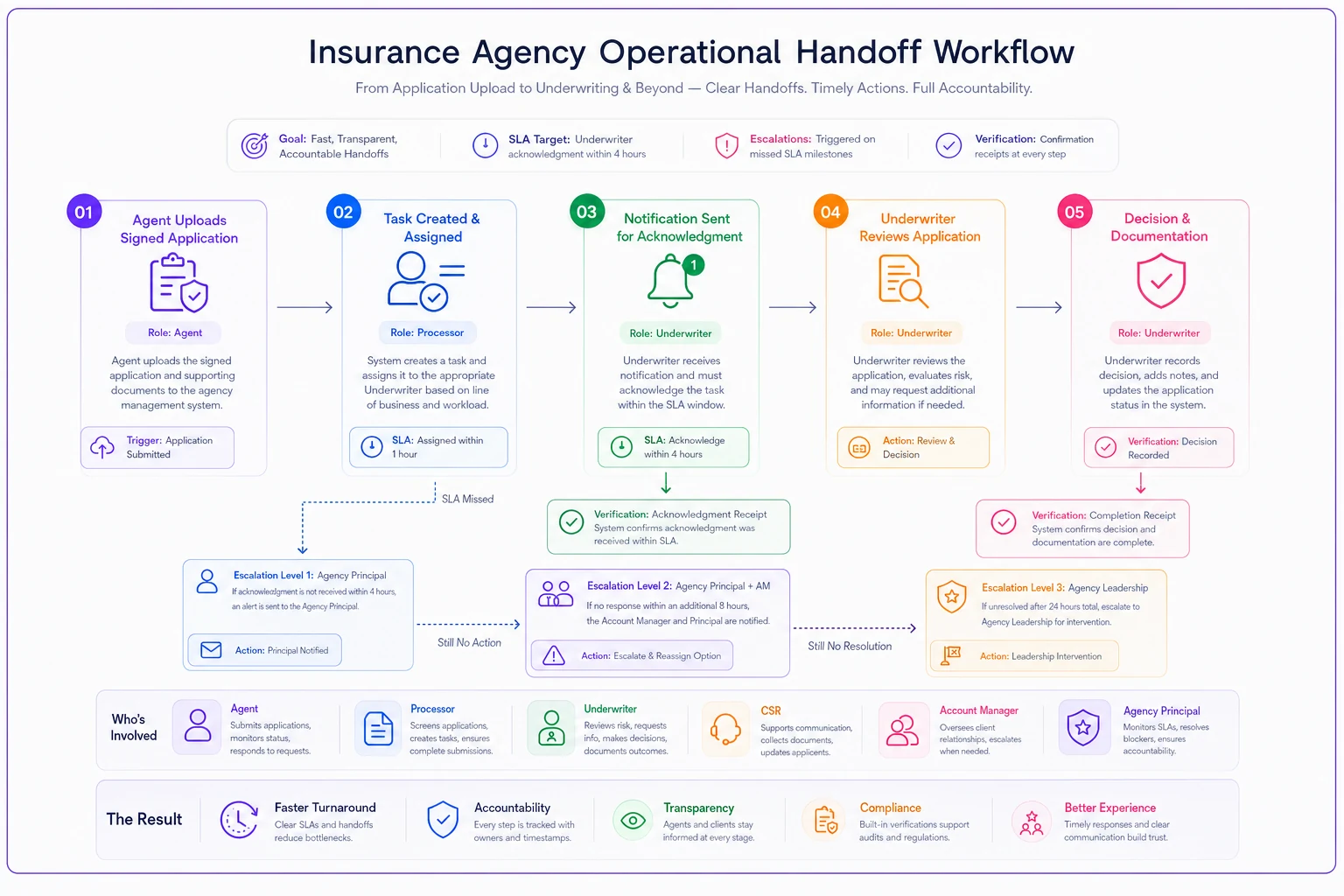

New Business Handoffs: When an application gets signed (trigger), the agent uploads it to the shared drive and assigns it in the management system to underwriting within 2 hours (action). The system sends a notification that requires acknowledgment within 24 hours (verification).

Renewal Processing Handoffs: Renewals hitting the 60-day mark automatically generate tasks for the assigned account manager. If no action is taken within 72 hours, it escalates to the agency principal. No exceptions.

Claims Coordination Handoffs: First notice of loss goes to the CSR, who creates the claim record and assigns it based on complexity. Personal auto goes directly to carriers. Commercial claims or anything over $25k gets assigned to an account manager within one hour. The handoff includes copying the original agent and requires confirmation of receipt.

Service Request Routing: Endorsement requests get categorized at intake: simple (address changes, vehicle swaps) go to CSRs with a 24-hour SLA. Complex (coverage changes, business classification updates) go to agents with a 48-hour SLA. Anything requiring underwriter review gets flagged and tracked separately.

Here's a simple visual of the handoff workflow.

The verification step is what most agencies miss. Without it, you're just creating more documentation that nobody follows. With it, you create accountability loops that make dropped handoffs visible immediately.

One mid-size agency in Virginia implemented this exact structure and saw their average policy processing time drop from 8 days to 3. Not because people worked faster, but because work stopped disappearing into the gaps.

Stage-specific KPIs that reveal operational health

Most agencies track the wrong metrics. Premium volume tells you about sales. Loss ratios tell you about underwriting. Neither tells you if your operations are healthy.

Operational health shows up in flow metrics—how smoothly work moves through your agency.

Quoting Stage KPIs:

-

Quote-to-bind ratio by producer (reveals sales effectiveness)

-

Average quote turnaround time (should be under 24 hours for standard risks)

-

Quotes requiring underwriter review (should be less than 30%)

-

Abandoned quote percentage (anything over 20% indicates process friction)

Binding Stage KPIs:

-

Bind-to-issue timeframe (target under 48 hours)

-

Binding errors requiring correction (should be under 5%)

-

Percentage of binds missing required documents (reveals intake problems)

Servicing Stage KPIs:

-

Service request completion time by type

-

Endorsements processed same-day (target 70% for simple changes)

-

Service requests requiring callbacks (under 15% indicates clear processes)

Renewal Stage KPIs:

-

Renewals reviewed 45+ days before expiration (target 85%)

-

Renewal retention rate by account manager

-

Remarketing success rate (reveals market relationships)

-

Lost renewals due to processing delays (should be zero)

Claims Stage KPIs:

-

First notice to carrier submission time (under 4 hours)

-

Claims requiring follow-up (under 20%)

-

Client satisfaction score post-claim

Track these KPIs by role, not just agency-wide. An account manager with a 95% renewal retention rate but only 60% reviewed before 45 days is heading for problems. A CSR completing simple endorsements in 2 hours but complex ones in 2 weeks needs better escalation rules.

Integration requirements that eliminate information silos

Every agency runs on a patchwork of systems that barely talk to each other. Your agency management system holds policy data. Your CRM tracks interactions. Your email contains the actual communication. Your phone system logs calls. Carriers have their own portals.

The successful agencies don't try to force everything into one system. They build bridges between systems at critical handoff points.

Critical Integration Points:

-

Your quoting tools need to push data to your management system automatically. Manual re-entry of quote data causes roughly 15% of binding errors and wastes about 20 minutes per policy.

-

Email needs to attach to client records automatically. The average commercial lines account generates 50+ emails annually. Without automatic attachment, critical information lives in individual inboxes where nobody else can find it.

-

Document management can't be optional. Every document needs to live in one central location, tagged by client and policy. The number of E&O claims that start with "we couldn't find the email where they declined that coverage" would shock you.

-

Task management must be role-based and integrated. When a renewal task gets created, it needs to appear in the assigned person's workflow immediately, not in some separate system they check twice a week.

-

Carrier downloads should be automated where possible. Manual downloading and entering of policies is where most data errors originate. If you're still having someone log into carrier portals daily to download policies, you're burning money and creating errors.

The Non-Negotiable: Single Source of Truth

Every piece of information needs one canonical location. Client contact information lives in the management system, not in someone's phone. Coverage details live in the policy system, not in Excel. Communication lives in the attached emails, not in random notepads.

Prioritize automating email-to-client record attachments early—it's high impact and low complexity.

When information exists in multiple places, people waste time figuring out which version is current. Worse, they make decisions based on outdated information.

Common failure points across the policy lifecycle

Agencies don't usually have single points of failure. They have failure patterns that repeat across multiple policies until someone notices the damage.

The Quote Black Hole Quotes get created but never followed up on. The producer assumes the prospect isn't interested. The prospect assumes the agency isn't interested. Meanwhile, competitor agencies stay persistent and win the business. About 30% of quotes die from lack of follow-up, not rejection.

The Renewal Scramble Renewals get noticed two weeks before expiration. Everyone drops everything to process them. Mistakes get made. Clients get upset about last-minute changes. This is completely preventable with proper staging and role assignment.

The Documentation Gap Policies get bound with verbal agreements to "get the documents later." Later never comes. Claims happen. Coverage disputes arise. Now you're trying to prove what was discussed in a phone call six months ago. This causes more E&O claims than any other operational failure.

The Handoff Assumption "I sent them an email" becomes the most dangerous phrase in your agency. Sending doesn't equal receiving. Receiving doesn't equal understanding. Understanding doesn't equal action. Every critical handoff needs confirmation, not assumption.

The Service Request Shuffle A client calls with a "simple" request. The CSR takes the message but isn't sure who handles it. They forward it to someone who forwards it to someone else. Three days later, the client calls again, angry that nothing happened. The request was actually completed day one—nobody told the client.

Building accountability without micromanaging

The word "accountability" makes most insurance professionals nervous because it usually means someone watching over your shoulder. But operational accountability isn't about surveillance—it's about visibility.

When everyone can see the status of work in the pipeline, accountability becomes automatic. The agent can see that their quote is waiting for underwriter review. The underwriter can see how many quotes are in their queue. The CSR can see which endorsements are approaching SLA limits.

This visibility needs to be role-appropriate. Agents don't need to see every service request. CSRs don't need to see every quote. But everyone needs to see the work they're responsible for and the work they're waiting on.

Accountability Mechanisms That Work:

-

Daily huddles focused on blockers, not status updates. "What's preventing you from completing your work today?" Not "tell me everything you're working on."

-

Weekly pipeline reviews by role. Agents review quotes and renewals. CSRs review service requests. Together, you identify patterns before they become problems.

-

SLA tracking with escalation. Not punishment for missing SLAs, but automatic escalation to get help. When a quote sits for 48 hours, it escalates to the sales manager. When a service request hits 24 hours, it escalates to the service manager.

-

Clear ownership assignment. Every piece of work has one owner at any given time. Not a committee, not a department—one person whose name is attached.

The best accountability system is one where people can see their own performance metrics. An agent who can see their quote-to-bind ratio naturally wants to improve it. A CSR who can see their service request completion time naturally tries to beat it.

Scaling the blueprint: From 5 to 50 employees

The blueprint that works for a 5-person agency breaks at 15 people. The one that works at 15 breaks at 30. Build flexibility into your operational structure from the beginning.

| Stage | Description |

|---|---|

| 5-10 Employee Stage: | 5-10 Employee Stage: Everyone wears multiple hats, but primary responsibilities are clear. The focus is on basic handoff rules and simple KPI tracking. You need shared visibility into all work, usually through a basic management system or even a sophisticated spreadsheet system. Integration isn't critical yet—manual processes still work at this scale. |

| 10-20 Employee Stage: | 10-20 Employee Stage: Role specialization becomes necessary. You need dedicated CSRs, possibly an account manager for larger clients. Handoff rules become critical. KPIs need to be tracked by role, not just agency-wide. This is where most agencies hit their first operational crisis—the informal coordination that worked before completely breaks down. |

| 20-35 Employee Stage: | 20-35 Employee Stage: Departments start forming naturally. Sales, service, and operations become distinct functions. You need team leads or managers for each function. Integration between systems becomes mandatory—manual handoffs can't scale anymore. This is where AI-powered operational software starts delivering massive returns by automating routine handoffs and tracking. |

| 35-50 Employee Stage: | 35-50 Employee Stage: Specialization deepens. You might have dedicated renewals processors, new business coordinators, claims specialists. The challenge becomes maintaining consistency across teams. Your operational blueprint needs governance—someone whose job is ensuring processes are followed and improved. |

The Scaling Secret: Don't wait until you hit the breaking point to implement the next stage's systems. If you have 8 employees, build for 15. If you have 18, build for 30. The cost of being slightly over-systemized is nothing compared to the cost of operational chaos during growth spurts.

Making it sustainable with AI-powered operational software

Modern tools change everything. The operational blueprint I've described would have required an army of managers to maintain five years ago. Today, AI automation handles the repetitive coordination that used to burn out your best people.

AI-powered operational software doesn't replace judgment—it replaces the mundane tracking and routing that consumes 30% of everyone's day. When a quote comes in, AI assigns it based on complexity and current workload. When a renewal approaches, AI creates tasks and monitors completion. When handoffs happen, AI ensures acknowledgment and tracks SLAs.

The agencies seeing the best results use AI for three specific functions:

Intelligent Routing: AI analyzes incoming work and routes it to the right person based on expertise, workload, and priority. No more guessing who should handle what.

Automated Tracking: Every handoff, every task, every deadline gets tracked automatically. You stop relying on people to remember to update systems.

Proactive Alerting: AI identifies when things are about to go wrong—quotes aging out, renewals running late, service requests approaching SLA limits—and alerts the right people before issues escalate.

One agency in Atlanta implemented AI-powered routing and tracking across their 22-person team. Within three months, their policy processing time dropped by 40%, not because people worked faster, but because work stopped getting lost between handoffs. Their CSRs spent less time figuring out who to route things to. Their agents stopped chasing status updates. Everyone focused on their actual job instead of coordination overhead.

The real power comes from AI learning your agency's patterns. It notices that certain types of commercial quotes always need underwriter review. It learns which account managers handle specific client types best. It identifies which handoffs frequently fail and suggests process improvements.

Conclusion: The difference between agencies that scale and those that struggle

Every agency owner I talk to wants to grow. Most think growth means more sales. But sustainable growth means building operations that can handle more volume without proportionally more chaos.

The agencies that successfully scale don't do it through heroic effort or by hiring amazing people who never make mistakes. They do it by acknowledging that policy lifecycle management for insurance agencies is fundamentally about coordination, not documentation.

They build clear role definitions that everyone understands. They create handoff rules that are impossible to ignore. They track KPIs that reveal problems before clients complain. They integrate systems at critical junction points. They make accountability automatic through visibility.

Most importantly, they recognize that their operational blueprint needs to evolve with their growth. The systems that got you to $5 million in premium won't get you to $15 million. The processes that work for 10 people break at 25.

The good news? You don't need to figure this out through trial and error anymore. Modern AI-powered operational software can implement these blueprints automatically, adapting as you grow. The agencies embracing these tools aren't just growing faster—they're growing without the operational debt that usually comes with scale.

Your next step isn't to rebuild everything at once. Pick one broken handoff—probably between sales and service—and fix it with clear rules and verification. Measure the impact. Then fix the next one. Within six months, you'll have transformed your operations from a collection of individual efforts into a coordinated system that scales.

The alternative is to keep hoping that hiring more people will solve your operational problems. But as anyone who's tried that approach knows, more people without better systems just means more chaos at a higher payroll cost.

Ready to transform your insurance agency operations?

Join 500+ agencies using Covixly to reduce manual work, improve client service, and grow their book of business.