A storm rolls through your service area and suddenly you're staring at hundreds of property damage claims from strip mall tenants, small manufacturers, and local retailers. Each one needs different handling, different urgency, different expertise.

Most agencies handle this surge exactly wrong. They treat every claim equally, dumping them all into the same queue. Senior adjusters waste hours on straightforward water damage claims while complex business interruption cases sit untouched for days. By the time someone catches the mistake, you've blown past SLAs and the client's already shopping for a new broker.

The real problem isn't the volume—it's the lack of systematic triage. Without clear routing rules and decision criteria, every claim becomes a judgment call. Your team burns mental energy on basic decisions instead of actually resolving claims.

Understanding the economics of small commercial claims processing

Small commercial claims occupy this weird middle ground in insurance operations. They're too complex for pure automation but too numerous for white-glove treatment. A typical agency processing around 2,000 small commercial claims annually faces some brutal math.

Your average claim touches 4-6 people before resolution. Initial intake, coverage verification, adjuster assignment, investigation, settlement negotiation, final documentation. At roughly 45 minutes of total handling time per claim, you're looking at about 1,500 hours of labor monthly just on processing. Factor in rework from mis-routed claims and that number jumps by another 20%.

The distribution breaks down predictably. Around 65% of small commercial claims are straightforward property damage—broken windows, minor water damage, equipment theft under $10k. Another 25% involve moderate complexity—multiple coverage questions, subrogation potential, or damages in the $10k-50k range. The remaining 10% are your nightmare scenarios—business interruption, liability disputes, or anything touching environmental damage.

Yet most agencies treat all three categories identically. They flow through the same intake process, hit the same review queue, get assigned to whoever's available.

Building your triage matrix: decision criteria that actually work

The core of effective claims triage isn't technology—it's clear decision logic. Binary criteria that anyone can apply consistently, not subjective judgment calls that change with every team member.

Eliminate paperwork bottlenecks and missed deadlines.

Covixly helps you track, manage, and close every policy and claim with confidence and speed.

- Unified policy & claims management

- Automated client notifications

- Agent task coordination

No credit card required

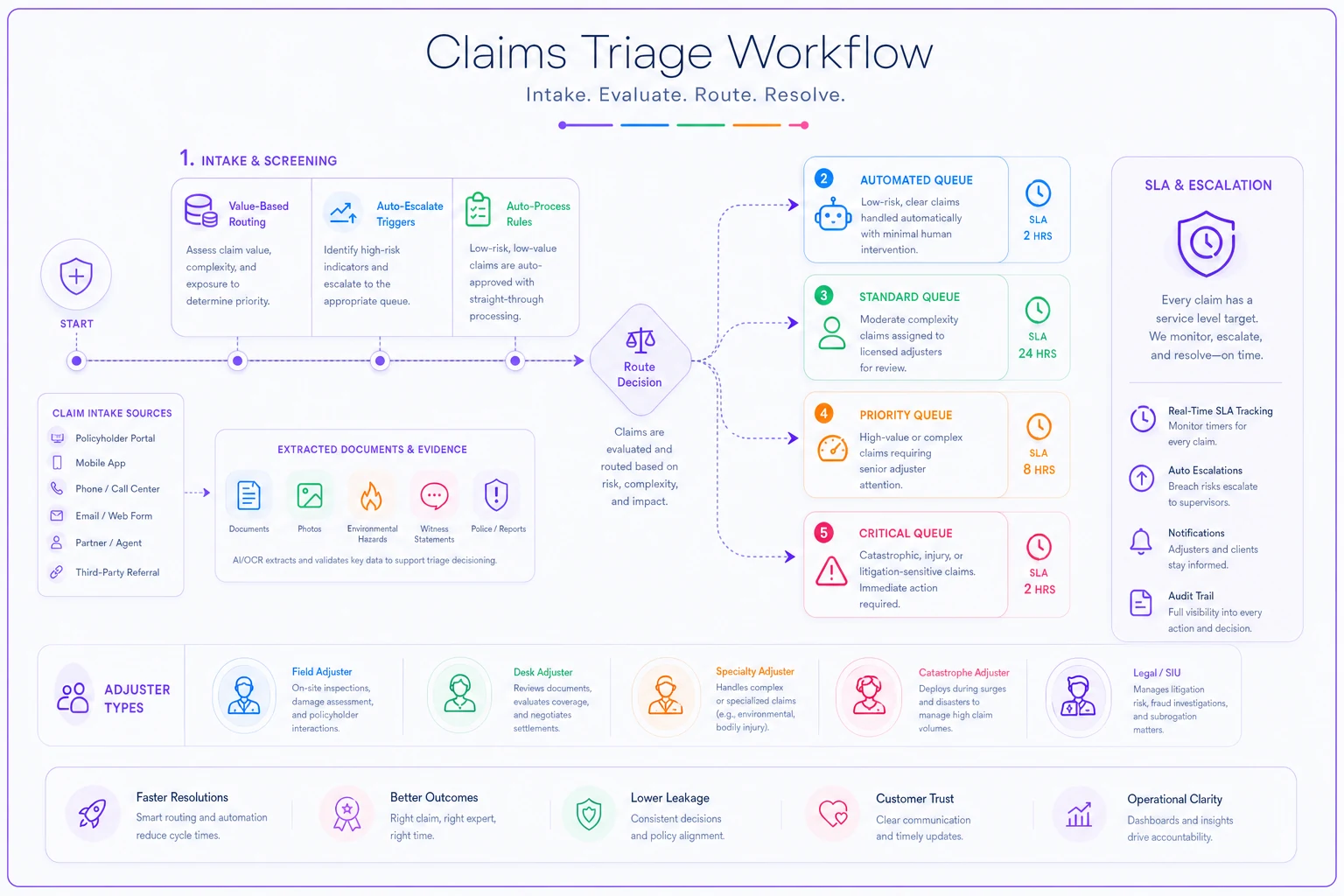

Start with claim value as your primary sort. Under $5,000? That's your automation tier. Between $5k-25k? Standard processing with junior adjusters. Over $25k or any bodily injury? Senior adjuster required. This simple three-tier system eliminates most routing decisions.

Next layer in complexity indicators. These are your escalation triggers that override value-based routing:

Auto-escalate criteria:

-

Any claim mentioning attorneys or litigation

-

Environmental damage (mold, asbestos, chemical spills)

-

Claims filed more than 30 days after loss date

-

Multiple claimants on single incident

-

Any government or municipal property involved

-

Claims where coverage is unclear or disputed

-

Business interruption exceeding 72 hours

Auto-process criteria:

-

Single-peril property damage under $5k

-

Equipment theft with police report attached

-

Glass/vandalism with photos submitted

-

Weather-related damage matching known event dates

-

First-party property claims with complete documentation

Binary criteria work because there's no interpretation needed. Either the claim mentions an attorney or it doesn't. Either damage exceeds $25k or it doesn't. Your intake team can route claims in seconds instead of deliberating for minutes.

The workflow below maps claim intake to routing decisions.

Use this workflow to train intake staff and automate simple routes.

SLA tiers that balance speed with resource reality

Generic 24-48-72 hour SLAs ignore operational reality. Small commercial claims need graduated response times based on actual business impact.

| **SLA Tier** | **Response Time** | **Claim Types** | **Volume %** | **Required Expertise** |

|---|---|---|---|---|

| Critical | 4 hours | Active business interruption, liability with injuries, environmental hazards | 5% | Senior adjusters only |

| Priority | 24 hours | Property damage $25k-100k, coverage questions, multi-location incidents | 15% | Experienced adjusters |

| Standard | 72 hours | Property damage $5k-25k, equipment claims, single-location events | 65% | Junior adjusters |

| Automated | Instant/7 days | Property damage under $5k, pre-approved repairs, glass/vandalism | 15% | System processing |

Maybe 5% of volume but potentially 40% of exposure for Critical tier claims. Missing these SLAs doesn't just upset clients—it creates actual liability. You need your best people on standby for these, even if it means overtime costs.

Priority tier represents roughly 15% of your volume. These need experienced adjusters but not emergency response. The 24-hour window gives you flexibility to batch assignments during normal business hours.

Standard tier is your bread and butter—around 65% of claims volume. The 72-hour SLA seems generous, but it allows for weekend incidents and gives adjusters time to properly investigate rather than rush through settlements.

Automated tier claims either process automatically through preset rules or get batched for weekly review.

Practical routing rules for real-world operations

Routing rules work best when they're dead simple. Complex decision trees create confusion and slow down processing.

Time-based routing:

-

Claims submitted before 2 PM → Same day assignment

-

Claims submitted after 2 PM → Next business day assignment

-

Weekend submissions → Monday batch processing

-

Holiday periods → Extended SLA automatically applied

Skill-based routing:

-

Environmental claims → Only adjusters with HAZMAT certification

-

Restaurant/food service → Adjusters with health code knowledge

-

Manufacturing claims → Industrial property specialists

-

Retail theft → Adjusters with inventory valuation experience

Geographic routing:

-

Urban claims → Field adjusters within 15-mile radius

-

Rural claims → Remote desk adjustment or regional adjuster

-

Multi-state claims → Corporate escalation team

-

CAT events → Dedicated storm team activation

Load balancing rules:

-

Maximum 15 active claims per junior adjuster

-

Maximum 8 complex claims per senior adjuster

-

Overflow triggers at around 80% capacity

-

Automatic redistribution when someone's out sick

Making these rules systematic, not suggestions, is what matters. When a restaurant fire claim comes in, it automatically routes to someone with food service experience. When a rural claim arrives, it goes straight to desk adjustment.

Resource allocation trade-offs you'll actually face

Perfect claims triage sounds great until you hit resource constraints. You've got 3 senior adjusters, 8 junior staff, and suddenly 200 weather-related claims drop on a Tuesday morning.

The first trade-off: automation versus accuracy. Those under-$5k claims you planned to auto-approve? Some will have hidden complexity. Maybe 2-3% involve coverage issues you'll miss. But manually reviewing all of them means your senior staff spends most of their time on low-value work.

Take one roofing company claim from last month. Storm damage, $4,200 estimate, looked perfect for auto-approval. Three weeks later we discovered the "storm" happened two months before they filed, and the real damage was from a contractor accident they were trying to shift. Cost another $6,000 to settle properly.

But that one mistake versus the dozens of routine claims processed correctly? The math usually favors accepting occasional errors over systematic inefficiency.

Second trade-off: speed versus thoroughness. Meeting aggressive SLAs means making decisions with incomplete information. You settle that $8,000 equipment claim quickly, then discover the damage was actually $14,000. Now you're reopening files and annoying clients.

Third trade-off: specialization versus flexibility. Dedicated routing by expertise sounds optimal until your restaurant specialist calls in sick during a week with twelve restaurant claims. Do you delay those claims for proper expertise or assign them to whoever's available?

Most agencies find the sweet spot around building depth in critical specializations and accepting generalist handling for everything else. Environmental claims always need experts. Restaurant grease fires? Maybe not so much.

Templates that eliminate decision fatigue

Templates remove cognitive load by pre-defining standard scenarios instead of requiring people to think through every routing decision.

Storm surge template:

-

All claims under $10k → Auto-approve with photo documentation

-

$10k-50k → Desk adjustment with vendor quotes

-

Over $50k → Field inspection required

-

Business interruption → Immediate escalation regardless of value

Theft/vandalism template:

-

Police report attached + under $5k → Auto-approve

-

Police report attached + $5k-25k → Standard tier desk adjustment

-

No police report → Hold pending documentation

-

Multiple locations affected → Escalate for pattern investigation

Water damage template:

-

Burst pipe with shutoff confirmed → Standard processing

-

Active leak → Critical tier response

-

Mold mentioned → Environmental escalation

-

Multiple floors affected → Senior adjuster required

Equipment breakdown template:

-

Under warranty → Vendor coordination process

-

Over warranty + under $10k → Replacement authorization

-

Over warranty + over $10k → Repair versus replace analysis

-

Production equipment → Business interruption assessment

These templates handle maybe 75% of your claims volume. Instead of analyzing each claim individually, your team just identifies the template and follows the predetermined path. A junior staffer can correctly route complex claims because the decision logic is built into the template, not their judgment.

Monitoring and adjustment mechanisms

Your triage matrix will be wrong at first. Agencies that succeed build in feedback loops from day one.

Track three key metrics religiously. First, rerouting rate—how often claims get reassigned after initial routing. Anything over 10% means your criteria need adjustment. Second, SLA breach patterns. If you're consistently missing SLAs on specific claim types, either your tiers are wrong or your capacity planning is off. Third, settlement variance by routing path.

Last quarter one agency noticed their auto-approved equipment claims were settling 15% higher than manually reviewed ones. Turns out their automation criteria were missing depreciation factors on older equipment. Quick fix, but it would've cost serious money if they hadn't caught it.

Weekly routing reviews catch problems before they cascade. Pull ten random claims from each tier and verify they were routed correctly. Look for patterns in the misrouted ones. Maybe your team doesn't understand what constitutes "environmental damage" or they're missing attorney involvement buried in claim notes.

Pull ten random claims from each tier during weekly routing reviews to catch problems early.

Monthly recalibration keeps your matrix aligned with reality. Review your tier thresholds against actual claim distributions. If 40% of claims now fall into Priority tier instead of the expected 15%, your thresholds need adjusting.

Proper claims triage creates cascading operational improvements most agencies never anticipate. Resolution velocity jumps immediately because claims land with the right expert on first assignment.

The compound effect of proper claims triage

Getting claims triage right creates cascading operational improvements most agencies never anticipate.

Resolution velocity jumps immediately. Claims that used to ping-pong between adjusters for days now land with the right expert on first assignment. That $3,500 equipment claim that used to take 5 days to settle now closes in 48 hours. Multiply that acceleration across hundreds of claims monthly and you're looking at dramatic working capital improvements.

Staff satisfaction improves because people work within their competency zones. Junior adjusters handle straightforward claims where they can build confidence. Senior adjusters focus on complex cases that actually use their expertise.

Client perception shifts even more dramatically. When that bakery owner files a claim for their damaged oven, they get a response in 4 hours because it triggered business interruption criteria. When the strip mall has minor vandalism, it processes automatically without consuming anyone's time.

The financial impact compounds over time. Proper triage reduces claim handling costs by 25-30% through better resource allocation. Settlement accuracy improves because the right expertise gets applied to each claim type. Litigation frequency drops because high-risk claims get senior attention before they escalate.

Modern operational software platforms can amplify these improvements by automating the routing decisions and tracking performance metrics. AI-assisted systems help identify patterns in claim characteristics and flag potential issues before they become problems.

Building your implementation roadmap

Rolling out a claims triage matrix isn't a flip-the-switch operation. Agencies that succeed phase their implementation to maintain stability while improving systematically.

Start with classification only. For the first month, don't change any routing—just track how claims would be classified under your new matrix. This surfaces gaps in your criteria and helps staff learn the classification logic without operational disruption.

One agency discovered they were getting way more environmental claims than expected during this phase. Turns out their intake team wasn't flagging anything mentioning "water damage in basement" as potential mold issues. Simple terminology training fixed it.

Next, implement automated tier only. Start routing just your simplest claims through automated approval. Monitor these carefully for two weeks. If error rates stay under 3%, expand the criteria slightly. If errors spike, tighten the rules.

Add manual tiers incrementally. Implement Standard tier routing first since it has the most forgiving SLAs. After two weeks, add Priority tier. Critical tier comes last because errors here have the biggest impact.

Templates roll out by frequency. Start with your most common claim type—probably weather-related property damage. Once that template works smoothly, add the next most common.

The full implementation typically takes 8-10 weeks. By week 12, you should see measurable improvements in resolution time, rerouting rates, and resource utilization.

AI-powered operational platforms can significantly accelerate this timeline by learning from your existing claim patterns and suggesting optimal routing rules based on historical data.

Common pitfalls that destroy triage effectiveness

Even well-designed triage matrices fail when implementation ignores operational reality.

Over-complex criteria kill adoption. When your routing rules require checking twelve different factors, people just give up and route based on gut feel. Your matrix needs to be simple enough that a new employee can accurately route claims on their first day.

Rigid SLAs that ignore business cycles cause systematic failures. That 4-hour Critical tier SLA sounds good until you realize 30% of these claims come in after 6 PM or on weekends. Now you're either staffing 24/7 support or constantly breaching SLAs.

Failure to maintain templates leads to gradual degradation. Your storm surge template works great for the first CAT event. By the third event, adjusters are freelancing because the template doesn't address some edge case they encountered. Without regular template updates based on actual events, your standardization erodes back to chaos.

Misaligned incentives undermine the entire system. If adjusters get bonused on claim count regardless of complexity, they'll cherry-pick easy claims while complex ones languish. If speed matters more than accuracy, your automation tier will approve claims it shouldn't.

The worst mistake is treating your triage matrix as a set-it-and-forget-it system. Claims patterns change with seasons, economic conditions, and regulatory shifts. What worked perfectly for your spring storm surge might fail completely during winter freeze claims.

Technology integration without complete automation

The right technology amplifies good triage without replacing human judgment. Most agencies get this balance wrong, either avoiding technology entirely or trying to automate everything.

Intake automation should handle data capture and initial classification. When a claim email arrives, automated text extraction pulls out key data points—claim value, date of loss, type of damage, business type. This pre-population eliminates 5-10 minutes of manual data entry per claim while reducing errors from mistyped information.

Workflow automation moves claims through your matrix without manual handoffs. Once classified, claims automatically route to the appropriate queue, SLA timers start, and notifications go to assigned adjusters.

But keep humans in the decision loop for anything complex. Automation should present information and recommendations, not make final decisions on coverage or settlement amounts. A system might flag that a claim matches auto-approval criteria, but a human confirms before payment processes.

AI-powered operational software helps by pattern matching and surfacing insights. It notices that claims from a particular zip code spike after storms, suggesting you pre-position resources there. It identifies that certain business types consistently under-report damages, recommending closer investigation.

The sweet spot is usually 30-40% full automation, 40-50% AI-assisted processing, and 20-30% purely manual handling for complex cases. This mix maintains quality while dramatically improving throughput.

Measuring success beyond basic metrics

Most agencies track claims closed and average settlement time, then wonder why their operations don't improve. Real triage effectiveness requires deeper operational metrics.

Rework rate tells you if initial routing works. Track how many claims require additional adjuster involvement after initial settlement. High rework usually means your triage criteria miss important complexity indicators. If 20% of auto-approved claims need manual review later, your automation criteria are too loose.

First-touch resolution rate indicates whether claims reach the right expertise immediately. When claims resolve without reassignment or escalation, your routing logic works. Below 70% first-touch resolution means your skill-based routing needs refinement.

Capacity utilization by tier shows if your resource allocation matches reality. If Priority tier adjusters run at 95% capacity while Standard tier sits at 60%, your classification thresholds need adjustment. Aim for roughly 75-80% utilization across all tiers—enough to be efficient without creating bottlenecks.

Settlement variance by path reveals if your different processing paths produce consistent outcomes. Auto-approved claims should settle within 5-10% of manually reviewed claims with similar characteristics. Larger variances indicate your automation criteria allow too much subjectivity.

Client effort score beats satisfaction for operational insight. Track how many times clients must follow up on claims, submit additional documentation, or clarify information. High effort scores mean your triage creates friction somewhere in the process.

Building an effective claims triage matrix takes time and iteration, but the operational benefits compound quickly. When done right, it transforms claims processing from reactive chaos into predictable, efficient operations. Your adjusters work smarter, clients get better service, and your agency handles volume surges without breaking.

Ready to transform your insurance agency operations?

Join 500+ agencies using Covixly to reduce manual work, improve client service, and grow their book of business.